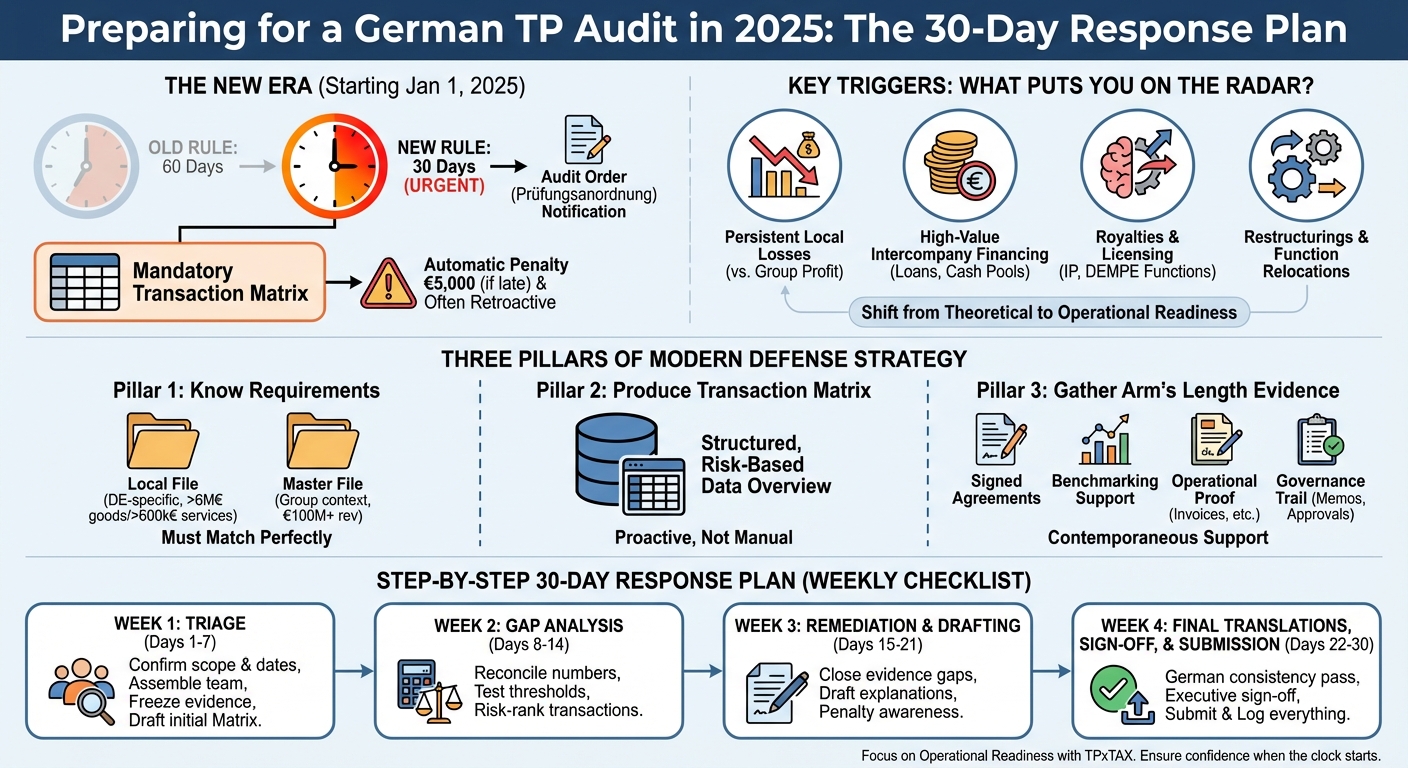

German transfer pricing (TP) audits move much faster starting January 1, 2025. If you receive an audit order (Prüfungsanordnung), the time to submit your TP documentation shrinks from 60 days to 30 days under the updated rules in Section 90 AO.

This is a complete shift from the old "get it ready during the audit" approach. Missing this deadline, especially for the new mandatory Transaction Matrix, triggers automatic surcharge penalties.

Here is a quick overview of the new rules:

- 30-Day Deadline: You have exactly 30 days to submit key TP documentation without a separate request.

- Transaction Matrix Requirement: A structured table detailing cross-border dealings is now mandatory to help authorities run risk-based scoring.

- Retroactive Scope: New 2025 audits will likely demand a Transaction Matrix for earlier years under review.

- Automatic Penalties: Failing to submit the Transaction Matrix on time triggers an automatic surcharge of EUR 5,000.

Preparing for these changes requires a shift from theoretical compliance to operational readiness. This guide covers what triggers an audit, the three pillars of a modern defense strategy, and a step-by-step 30-day response plan to help you stay compliant.

The New Era of German TP Audits

The 30-day clock is not just a tweak to the deadline, it changes how audits are staffed and targeted. Tax authorities are moving toward structured data to improve their audit efficiency.

The Transaction Matrix (Transaktionsmatrix) enables risk-oriented case selection. In other words, it helps the tax auditor decide where to look first. Because a 2025 audit order will often cover earlier tax years, you might need to create this matrix retroactively for those prior periods. Waiting to build it until the audit begins is no longer a safe option.

At the same time, Germany is sharpening its cross-border audit coordination. The BMF's updated guidance on audit cooperation explicitly mentions joint and simultaneous audits involving the Federal Central Tax Office (BZSt).

The practical takeaway for tax leaders is that TP readiness must be operational. A 30-day deadline leaves no time for data scrambling. Setting up a software-enabled workflow to maintain transaction data, documentation status, and audit-ready outputs continuously is the best way to transform an audit announcement into a controlled submission workflow.

Key Triggers: What Puts You on the Auditor's Radar?

German TP audits rarely start with a single transaction. They usually begin with a pattern where the numbers in the German entity do not match its people, decision-making, and value creation. The auditor then works backwards from there.

1) Persistent Local Losses

If the German entity shows recurring losses or consistently underperforms peers, expect a challenge to the story in your Local File. The auditor will question why Germany is the routine risk-taker on paper while the residual profit sits elsewhere.

Typical audit angles include:

- Limited-risk labels versus real-world conduct: Who actually controls key risks, makes the calls, and has the capability to manage them?

- Year-end adjustments: Auditors look for adjustments that appear to be outcome-based profit steering instead of arm's-length pricing, especially if the loss-making entity is trued up every year.

- Benchmark selection: The rejection of loss makers, comparability filters, and multi-year versus single-year results will be scrutinized.

Monthly or quarterly margin monitoring helps defensibly. A clean tie-out from your ERP system to the transaction set allows you to explain losses fast, before the auditor fills the gaps with their own narrative.

2) High-Value Intercompany Financing

Financing is a major audit topic. Tax authorities expect documented debt capacity and business purpose for loans, cash pools, and guarantees. They will scrutinize whether the interest rate exceeds what the borrower could obtain based on the group rating.

Practical red flags in audits include:

- Back-to-back or conduit lenders that look low-function and low-risk but retain a large spread.

- Weak evidence regarding credit rating, covenants, terms, and third-party comparables.

- Cash pool outcomes that do not match the participant's risk and benefit profile.

3) Royalties and Licensing

Large, rising, or newly introduced royalty payments (especially outbound from Germany) trigger immediate questions. The auditor wants to know what IP is being licensed, who manages the DEMPE functions, and why the German entity is not entitled to more return.

Expect the auditor to test whether the German entity effectively owns or enhances intangibles in substance, even if the legal ownership sits abroad.

4) Restructurings and Function Relocations

When you shift a German entity from an entrepreneur to a contract manufacturer or distributor, move key people, or relocate decision rights, auditors look for a "transfer package." They expect to see proper valuation logic, not just updated intercompany contracts. The BMF's Administrative Principles strictly address function relocations (Funktionsverlagerung) and how they must be analyzed.

The Three Pillars of German TP Defense

German audits now test speed and structure as much as pricing. A workable defense approach relies on three key pillars: knowing exactly which files you must have, producing a clean Transaction Matrix, and showing contemporaneous evidence that your outcomes were arm's length.

Pillar 1: Knowing the Local and Master File Requirements

Local File (Germany-specific documentation): This is required if cross-border related-party goods exceed EUR 6 million or services and other transactions exceed EUR 600,000 per year. Once triggered, the expectations are transaction-by-transaction documentation depth, rather than a light summary. Treat the Local File as your tailored audit narrative.

Master File (group-level documentation): This applies if you are part of a multinational enterprise group and the German entity's prior-year revenues reach the established threshold (typically EUR 100 million). The Master File serves as the group context and must perfectly match the Local File with no contradictions regarding the value chain, intangibles, or financing.

Pillar 2: Producing the Transaction Matrix

Starting in 2025, the Transaction Matrix is a standalone compulsory element. It acts as a structured, tabular overview of cross-border dealings with related parties and permanent establishments.

The BMF provides templates for single-year and multi-year reporting. While deviations are allowed in principle, they should be coordinated early to avoid format disputes. Remember that the matrix can become retroactive in practice, covering pre-2025 years if those years fall under the audit scope.

Building the matrix manually within a 30-day window is a high-risk strategy. A scalable approach involves building the matrix proactively from ERP data, intercompany agreements, and TP policy metadata so updates are incremental.

Pillar 3: Gathering Evidence of Arm's Length Outcomes

German auditors will ask what you knew when you set the price and how you monitored it. Your defense file behind the numbers should include:

- Signed intercompany agreements: Ensure these align perfectly with actual conduct regarding functions, risks, and terms.

- Benchmarking support: Document your screening logic, comparability adjustments, and refresh cadence.

- Operational proof: Keep records of invoices, service descriptions, benefit tests, and time-writing where relevant.

- Governance trail: Maintain a log of pricing memos, approval minutes, year-end true-up logic, and internal controls.

Operationalizing this as a living, audit-ready repository helps you respond quickly and consistently when the clock starts.

The 30-Day Response Plan (Step-by-Step Checklist)

A German Betriebsprüfung typically starts with a Prüfungsanordnung. From its notification date, the clock runs fast. Certain TP documents (including the Transaction Matrix) must be provided within 30 days without a separate request in many cases. The tax authority can also request TP records outside an external audit with the same 30-day submission concept.

Here is a weekly checklist to manage the response process.

Week 1: Triage (Days 1 to 7)

Goal: Stop uncontrolled data pulls and align on what must be delivered in 30 days.

- Confirm scope and dates: Verify which years and entities are covered by the Prüfungsanordnung. Map your milestones back from the exact calendar date of the 30-day deadline.

- Stand up a response team: Assemble a core team including tax (as the owner), controlling, ERP and data specialists, legal for contracts, and local German speakers for audit correspondence.

- Freeze and inventory evidence: Secure intercompany agreements, invoices, management accounts, segment P&Ls, price lists, and transfer pricing policies.

- Build the audit-front package: Create a working draft of the Transaction Matrix that gives the auditor a quick, risk-oriented overview.

Week 2: Gap Analysis (Days 8 to 14)

Goal: Identify exposure early and prioritize items that drive adjustments.

- Reconcile numbers: Ensure totals in the Transaction Matrix align perfectly with statutory accounts, management reporting, and TP calculation files to present one version of the truth.

- Test thresholds and deliverables: Confirm Local File triggers based on cross-border goods and services volumes, and determine exactly what must be ready by day 30.

- Risk-rank transactions: Prioritize high-risk areas like royalties, management services, IP and DEMPE fact patterns, business restructurings, losses, and year-to-year margin swings.

Week 3: Remediation and Drafting (Days 15 to 21)

Goal: Remediate weak spots and draft the final response package.

- Close evidence gaps: Search for missing contracts, perform benefit tests for services, verify allocation keys, lock in benchmarking support, and prepare segmented P&Ls.

- Draft audit-ready explanations: Create short, consistent narratives detailing the fact patterns and pricing mechanics for each transaction category.

- Penalty awareness: Remember that late or insufficient documentation can trigger penalty surcharges, including minimum amounts and per-day late fees.

Week 4: Final Translations, Sign-Off, and Submission (Days 22 to 30)

Goal: Submit clean, consistent German-language materials on time.

- German consistency pass: Verify that terminology, entity names, transaction labels, and cross-references match perfectly between German and English versions.

- Executive sign-off: Align the CFO and VP of Tax on the positions taken and acceptable settlement ranges.

- Submit and log everything: Document exactly what was provided, when it was sent, and in which format to build a foundation for follow-up questions in your audit defense file.

How TPxTAX Reduces Audit Heat

Treat preparing for an audit like a 30-day data-to-document pipeline. TPxTAX pairs senior TP advisory with software-enabled execution. This creates a transaction-level map that is immediately ready for the Transaction Matrix and Local File. By enabling automated tie-outs and proactive profitability monitoring, TPxTAX ensures that when the 30-day clock starts, you are confident in explaining facts instead of scrambling to find them.

Frequently Asked Questions

How many days do you have to respond to a German transfer pricing audit request?

Starting January 1, 2025, you have exactly 30 days from the notification of the audit order (Prüfungsanordnung) to submit your key transfer pricing documentation, including the newly mandatory Transaction Matrix. The old standard was 60 days.

What are the penalties for TP non-compliance in Germany?

Missing the 30-day deadline for the Transaction Matrix triggers an immediate and automatic surcharge of EUR 5,000 under Section 162(4) AO. This is separate from any adjustment-based penalties or standard per-day late fees that may apply for missing or insufficient Local and Master Files.

What is the new German Transaction Matrix (2025)?

The Transaction Matrix (Transaktionsmatrix) is a structured, tabular overview of all cross-border dealings with related parties and permanent establishments. It is now a standalone compulsory element designed to help the tax authorities run risk-based scoring to select audit targets efficiently.

Do I have to translate my TP documentation to German?

While English is commonly accepted for the Master File, German auditors legally have the right to demand German-language materials for the Local File and supporting evidence. It is highly recommended to do a "German consistency pass" on all terminology, entity names, and transaction labels before your 30-day submission window closes.