The Ultimate Guide to Pillar Two Global Minimum Tax (2026)

Pillar Two is no longer a "watchlist topic". For in-scope multinational groups, it is now an operating requirement touching tax, finance, controllership, legal, and data teams.

If your group is above the €750 million threshold, this guide gives you the practical playbook: what rules apply, what Germany expects under MinStG, how to calculate jurisdictional ETR, and what to file by when.

TL;DR: What Tax Leaders Need to Decide Now

- Confirm scope across the group and jurisdictions where you have Constituent Entities.

- Set rule-order logic in your process: QDMTT first, then IIR, then UTPR.

- Build a jurisdiction-by-jurisdiction ETR workflow with documented adjustments, not ad-hoc spreadsheets.

- Lock filing governance for Group Head Notification, GIR, and local minimum tax returns.

- Run safe harbor testing early to reduce unnecessary full-calculation effort.

- Align TP, CbCR, and Pillar Two datasets before deadlines to avoid reconciliation failures.

- Use an advisory-led execution model if internal capacity is limited; Pillar Two is a cross-functional delivery challenge, not just a filing task.

Pillar Two Global Minimum Tax Webinar

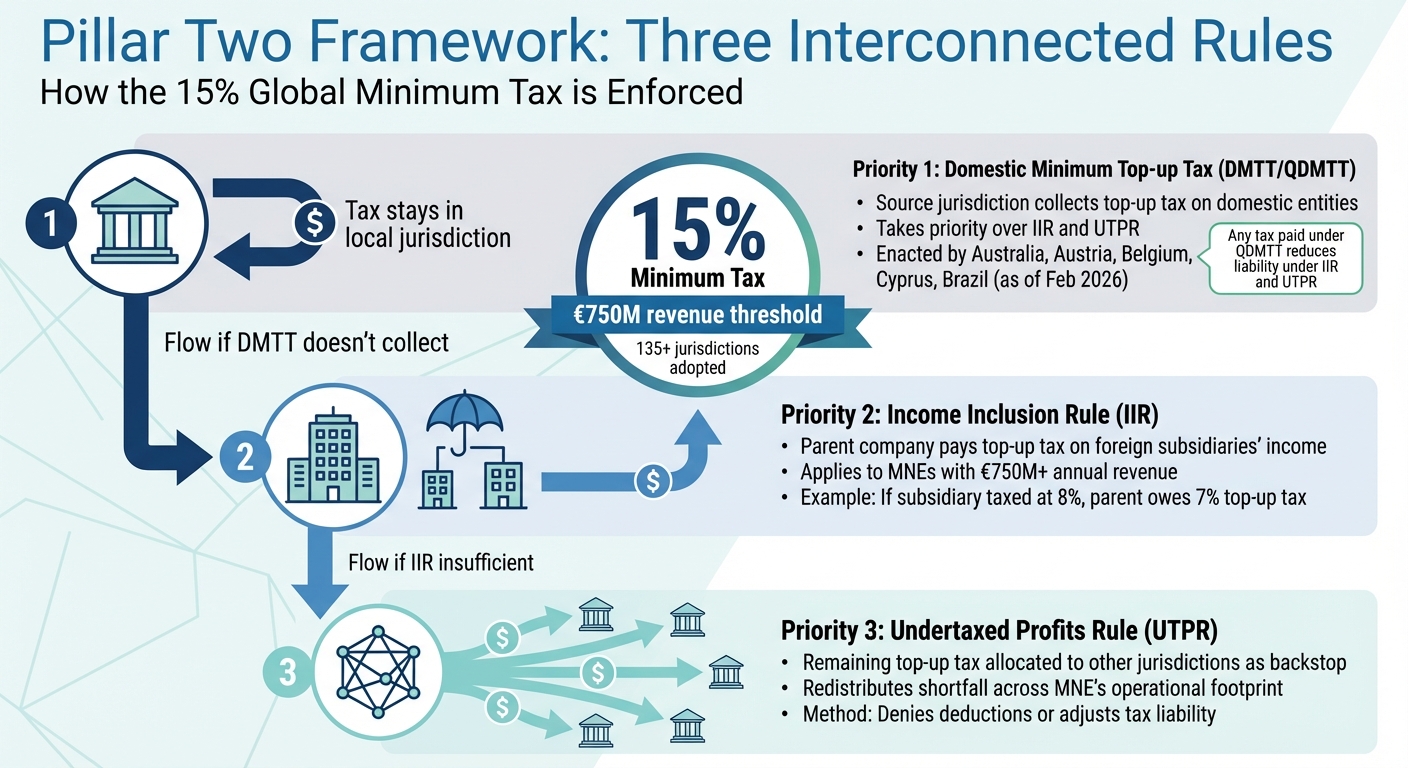

Pillar Two Framework in One View

The OECD GloBE framework enforces a 15% minimum effective tax rate (ETR) by jurisdiction for in-scope MNE groups. It works through three linked rules with a strict priority order.

| Rule | Priority | Practical effect |

|---|---|---|

| QDMTT / DMTT | 1st | Local jurisdiction collects top-up tax first on low-taxed local profits |

| IIR | 2nd | Parent-level inclusion of top-up tax if low-taxed profits remain |

| UTPR | 3rd | Backstop allocation across jurisdictions if top-up tax is still uncollected |

Income Inclusion Rule (IIR)

The IIR requires the parent jurisdiction to collect top-up tax when a subsidiary jurisdiction falls below 15% ETR (after GloBE adjustments). In practice, the IIR is your main parent-level charging rule.

Undertaxed Profits Rule (UTPR)

The UTPR applies only when the top-up amount is not fully captured under the IIR. It reallocates tax collection rights to other implementing jurisdictions.

Domestic Minimum Top-up Tax (QDMTT/DMTT)

A Qualified Domestic Minimum Top-up Tax (QDMTT) allows the source country to collect top-up tax domestically before another jurisdiction does. For many groups, QDMTT status by jurisdiction is now one of the most important annual tracking items.

Germany MinStG: What Is Already Live

Germany implemented Pillar Two through the Minimum Tax Act (Mindeststeuergesetz, MinStG), with core rules effective from fiscal years starting after 30 December 2023.

Key Germany Milestones

| Item | Date / Timing |

|---|---|

| MinStG publication | 27 December 2023 |

| IIR + DMTT generally effective | FYs beginning after 30 December 2023 |

| UTPR generally effective | FYs beginning after 30 December 2024 |

| First GIR (transition year) | 18 months after FY end (often 30 June 2026 for FY 2024 calendar-year groups) |

| Ongoing GIR deadline | 15 months after FY end |

Germany also operates with a Group Parent / Group Head filing concept under MinStG, which centralizes registration, filing, and payment obligations.

How ETR Is Calculated Under Pillar Two

At a high level:

Jurisdictional ETR = Adjusted Covered Taxes / Net GloBE Income

If the jurisdictional ETR is below 15%, top-up tax is calculated on the shortfall (subject to applicable exclusions and safe harbors).

Data Building Blocks You Need

- Financial accounting baseline per entity and jurisdiction

- GloBE income adjustments (including required exclusions and reclassifications)

- Adjusted covered tax logic (including deferred tax treatment rules)

- Jurisdictional blending across in-country entities

- Audit trail for every adjustment, including source-system lineage

Common ETR Failure Points

- Treating Pillar Two as a consolidation-only exercise with no entity-level controls

- Missing deferred tax adjustment documentation

- Failing to reconcile TP true-ups and CbCR data into the same period logic

- Manual spreadsheet overrides without approval history

Safe Harbors and Reliefs: Use Them Deliberately

Safe harbors can reduce compliance burden, but only if tested and documented correctly.

Transitional CbCR Safe Harbor

Can provide temporary relief from full GloBE computations in eligible jurisdictions if threshold tests are met (for example de minimis or simplified ETR tests, depending on period and guidance).

QDMTT Safe Harbor

Where a jurisdiction has a qualifying domestic minimum tax and required conditions are met, top-up may be treated as collected domestically for GloBE purposes.

Substance-Based Income Exclusion (SBIE)

SBIE reduces the excess profit base subject to top-up through payroll and tangible-asset carve-outs. Transition percentages step down over time; confirm year-specific rates before filing.

Filing Requirements: What Must Be Submitted

For in-scope groups in Germany, the compliance package usually includes:

- Group Head Notification

- GloBE Information Return (GIR)

- Minimum Tax Return (local filing route)

| Filing | Typical Recipient | Transition Timing (FY 2024 example) | Ongoing Timing |

|---|---|---|---|

| Group Head Notification | BZSt | 28 February 2025 | 2 months after tax period end |

| GIR | BZSt | 30 June 2026 (for many FY 2024 calendar-year groups) | 15 months after FY end |

| Minimum Tax Return | Local tax office pathway | Generally aligned with transition GIR logic | Generally aligned with ongoing GIR logic |

Always confirm final deadlines by entity and jurisdiction, especially where fiscal years differ from the calendar year.

Operating Model: How Mature Teams Execute Pillar Two

The strongest Pillar Two programs treat compliance as a managed process, not a one-off technical memo.

Governance

- Named owner for each jurisdiction package

- RACI between tax, finance, legal, and IT

- Version control and sign-off checkpoints before filing

Data and Controls

- Standardized chart-of-accounts to GloBE mapping

- Rules library for recurring adjustments

- Validation checks before GIR extraction

Policy and Planning

- Annual elections and interpretation log

- Scenario modeling for restructurings, financing, and IP changes

- Audit-defense file with reproducible calculations

TPxTAX Role in Pillar Two Compliance

TPxTAX is not a standalone software tool. TPxTAX is a transfer pricing and international tax advisory partner that combines:

- Senior tax specialists for rule interpretation and policy decisions

- Structured data workflows for calculation and filing readiness

- Delivery support for GIR preparation, review, and submission coordination

- Planning support for safe harbors, elections, and cross-border structuring implications

This model is useful for groups that need speed and rigor without building a large permanent Pillar Two delivery team internally.

90-Day Pillar Two Action Plan

Days 1-30: Scope and Design

- Confirm in-scope entities and jurisdictions

- Map QDMTT/IIR/UTPR applicability by jurisdiction

- Define target operating model and accountability

Days 31-60: Build and Test

- Build jurisdictional ETR packs and adjustment logic

- Run safe harbor testing and document decisions

- Reconcile TP, CbCR, and Pillar Two data cuts

Days 61-90: Govern and Execute

- Dry-run GIR data package

- Finalize sign-off workflow and controls

- Prepare filing calendar and authority-response protocol

FAQs

Does Pillar Two apply to every multinational?

No. The core entry test is the €750 million consolidated revenue threshold, plus scope mechanics under GloBE rules and local implementation.

What is the most important technical concept for execution?

Jurisdictional ETR accuracy. Most downstream top-up tax and filing risk comes from incomplete or inconsistent ETR inputs.

Is QDMTT optional to track if we already run IIR?

No. QDMTT status directly affects priority of collection and can materially change where tax is paid.

What is the biggest process risk?

Late reconciliation across tax, finance, and reporting data. By the time GIR assembly starts, core data design decisions should already be locked.

How should we position internal ownership?

Treat Pillar Two as an ongoing compliance capability with annual refresh cycles, not a one-time project.

Next Step for Tax Teams

If you need support designing or executing your Pillar Two compliance model, TPxTAX can help with advisory-led implementation, data workflow design, and filing readiness across jurisdictions.