Transfer Pricing Compliance Checklist for 2026

Transfer pricing compliance in 2026 is documentation plus execution plus audit readiness across Action 13, operational controls, Amount B, and Pillar Two reporting.

Download the checklist (free): 2026 Transfer Pricing Compliance Checklist

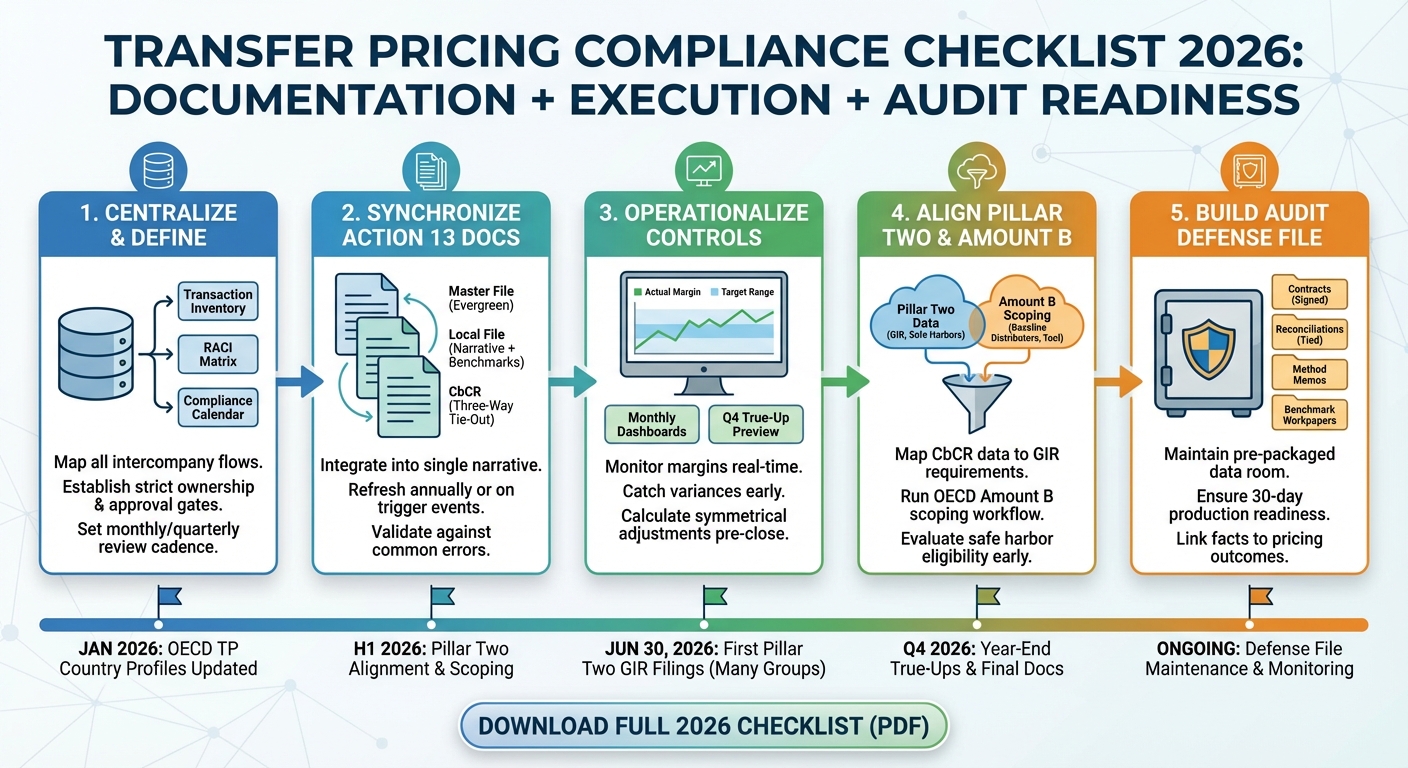

TL;DR: 5 Steps to Bulletproof Compliance in 2026

- Centralize your transaction inventory to stop chasing data out of fragmented systems and establish strict RACI guardrails.

- Synchronize Action 13 documentation (Master File, Local File, CbCR) into a single evergreen narrative to cut reporting bottlenecks.

- Operationalize real-time margin monitoring to catch variances early, eliminating the risk of year-end true-ups that trigger tax audits.

- Align Pillar Two and CbCR data early (and evaluate any transitional safe harbors) while running an Amount B scoping workflow for baseline distributors.

- Build an audit-ready defense file by pre-packaging your contracts, reconciliations, and benchmark workpapers into a central data room you can produce in 30 days.

Best use: Share with tax/finance/legal. Populate the inventory, assign owners, set the calendar.

What changed recently: The OECD updated its Transfer Pricing Country Profiles in January 2026 and continues to publish updates on Pillar One – Amount B. Many groups also face first Pillar Two GIR filings in 2026 (often June 30, 2026 for FY 2024 calendar-year groups), but deadlines vary by jurisdiction.

Quick-Reference Checklist

| Workstream | What to do | Owner | Frequency | Key evidence |

|---|---|---|---|---|

| Transaction inventory | Map all intercompany flows by type, entity, jurisdiction | Tax / TP team | Annual + mid-year trigger review | Transaction matrix, ICA register |

| Master File | Update for restructurings, DEMPE changes, financing shifts | Tax / TP team | Evergreen (annual sign-off) | Version-controlled MF document |

| Local File | Refresh narrative + benchmarking per transaction | Tax / TP team | Annual per entity | Functional analysis, benchmark workpapers |

| CbCR | Three-way tie-out (CbCR vs. LF vs. MF), validate 28 OECD common errors | Tax + Finance | Annual, pre-filing | Reconciliation workpapers |

| Operational TP (OTP) monitoring | Compare actual margins to arm's length targets | Finance / FP&A | Monthly dashboards, quarterly formal review | Margin reports, variance logs |

| Year-end true-ups | Calculate adjustments before close; book symmetrically | Tax + Finance | Q4 / pre-close | Debit/credit notes, ICA clauses |

| Amount B scoping | Run OECD Pricing Automation Tool for qualifying distributors | Tax / TP team | Annual (monitor tool/FAQ updates) | Tool output, scoping memo |

| Pillar Two alignment | Map CbCR data to GIR requirements; confirm safe harbor eligibility | Tax + Finance | H1 2026 (first GIR filings in 2026 for many groups) | GIR data package, safe harbor test |

| Defense file | Maintain indexed, version-controlled data room | Tax / TP team | Ongoing | Reconciliations, contracts, method memos |

1. Define Scope, Owners, and a 2026 Compliance Calendar

Build a Transaction Inventory With a Materiality Lens

Every defensible transfer pricing program starts with knowing what you have. A transaction inventory catalogs every cross-border related-party flow by type, counterparties, jurisdictions, volume, pricing method, and governing intercompany agreement.

Categories to capture:

- Tangible goods -- buy-sell, commissionaire, limited-risk distributor arrangements.

- Services -- management fees, shared services, technical services. Separate low-value-adding services (OECD Chapter VII simplified approach) from higher-value services needing full benchmarking.

- IP / royalties -- licenses for trademarks, patents, know-how. Map against the DEMPE framework.

- Financial transactions -- intercompany loans, cash pools, guarantees, captive insurance.

- Business restructurings -- function/asset/risk transfers, conversions to limited-risk models.

Use a pragmatic tiered approach:

- Tier 1 -- Full documentation: high-risk and high-value transactions (IP transfers, restructurings, loss-making entities, financing).

- Tier 2 -- Simplified documentation: mid-range transactions with streamlined benchmarking.

- Tier 3 -- Monitor only: low-value flows documented in the matrix with a brief pricing rationale.

Assign Owners and Set Approval Gates

Transfer pricing is cross-functional. Without clear ownership, intercompany agreements go unsigned, pricing changes happen without tax review, and year-end adjustments arrive too late.

A RACI matrix clarifies who does what:

| Activity | Tax / TP | Finance | Legal | Business Unit |

|---|---|---|---|---|

| TP policy design, method selection | A | C | C | I |

| Intercompany agreement drafting | C | I | A | I |

| Setting provisional transfer prices | R | R | I | C |

| Monthly/quarterly margin monitoring | C | R | I | I |

| Year-end true-up calculation | A | R | C | I |

| Documentation (MF/LF) | A/R | C | I | C |

| CbCR data gathering and filing | A | R | I | I |

*A = Accountable, R = Responsible, C = Consulted, I = Informed*

Four approval gates prevent unreviewed pricing from entering the system:

- New transaction approval -- TP team sign-off before the first invoice.

- Pricing-change approval -- TP team review when tariffs, FX, or restructurings drive mid-year changes.

- Year-end adjustment approval -- joint sign-off from tax (arm's length substance) and finance (accounting treatment, VAT/customs impact).

- ICA renewal -- annual review of intercompany agreements. Expired or stale agreements are a common audit trigger.

Set a 2026 Compliance Calendar

Monthly: Post intercompany transactions per TP policies. Run margin-monitoring dashboards. Flag entities trending outside target ranges.

Quarterly: Perform a formal margin review. Compare YTD results to arm's length ranges and decide whether a mid-year pricing adjustment is warranted. Review the transaction inventory for new or changed flows. Update the ICA tracker for expiring agreements.

Year-end (Q4 2026 into early 2027): Run Q3/Q4 margin previews to estimate true-up size. Calculate and post adjustments before close. Finalize FY 2025 documentation if not yet complete. Refresh benchmarking studies where the three-year cycle has elapsed.

Key external dates for 2026:

| Date | Event |

|---|---|

| Jun 30, 2026 | Common first GIR deadline for many calendar-year groups' FY 2024 filings (transition timing varies by jurisdiction) |

| Dec 31, 2026 | Many CbCR filings due within 12 months after FY 2025 year-end (confirm local deadlines); EU Public CbCR varies |

2. Refresh Action 13 Documentation (Master File, Local File, CbCR)

The three-tiered documentation framework under OECD BEPS Action 13 remains the backbone of global transfer pricing compliance. But "having documentation" and having documentation that holds up under audit scrutiny are different things.

Master File: Update Triggers and the Evergreen Approach

The Master File covers five categories: organizational structure, business descriptions, intangibles, intercompany financial activities, and consolidated financial/tax positions. It is meant to be a blueprint, not an exhaustive inventory.

Events that should trigger a substantive refresh:

- Group restructuring -- mergers, acquisitions, divestitures, entity creation/dissolution.

- Value chain realignment -- shifts in where functions are performed, risks assumed, or assets deployed.

- DEMPE changes -- any transfer or shift in Development, Enhancement, Maintenance, Protection, or Exploitation functions for intangibles. This is the primary audit focus for most tax authorities.

- Financing structure changes -- new intercompany loans, guarantee structures, cash-pooling arrangements.

- New TP policies or method changes -- adopting a new methodology for a transaction category.

Best practice is an evergreen, version-controlled Master File with a formal annual sign-off (and event-driven updates when facts change).

Local File: Build a Transaction-by-Transaction Story

The most common Local File failure is a “checkbox” functional analysis. Examiners expect your facts to clearly connect to method selection and pricing outcomes (IRS TP documentation FAQs).

Each controlled transaction in the Local File should read as a self-contained story:

- Business context -- what the entity does, why this intercompany transaction exists.

- Functional analysis -- who contributes what, who bears which risks, who owns which assets.

- Method selection -- given these facts, why this method produces the most reliable result. Explain why alternatives were rejected.

- Benchmarking result -- the arm's length range and where the tested party falls.

Benchmarking refresh: Refresh the full comparable search every three years and update financials annually. Refresh earlier if facts change (business model shift, disruption, comparables change, or method changes), and document *specific* accept/reject reasons.

CbCR: Tie-Outs, Appropriate Use, and Common Errors

CbCR is a risk-assessment tool, not a substitute for transaction-level TP analysis (OECD Guidance on Appropriate Use). In practice, anomalies often trigger follow-up Local File requests.

Run these cross-checks before filing:

- CbCR vs. Local File -- revenue, profit before tax, headcount reconcile; document consolidation adjustments.

- CbCR vs. Master File -- narrative must match the profit pattern (avoid “routine” labels with outlier profits).

- Revenue classification -- unrelated + related must equal total (OECD common errors).

- Employee allocation -- show where people actually work.

- Entity completeness -- every consolidated entity appears in Table 2.

Before filing, validate against the OECD’s common-errors checklist (employees, revenue totals, rounding, TINs, and permanent establishment naming are frequent issues).

Jurisdiction scan: Use the OECD TP Country Profiles (updated January 2026) to confirm local documentation expectations, dispute resolution, and any simplifications/safe harbors.

3. Operational Transfer Pricing: Controls That Prevent Ugly True-Ups

Monitoring Cadence and Thresholds

Operational TP (OTP) is not “set and forget.” Build a monitoring cadence that catches variances early:

- Monthly: dashboard actual vs. target margins; flag outliers and data issues.

- Quarterly: formal variance review; decide whether to make prospective pricing changes; run a Q3/Q4 preview.

- Thresholds: define tolerance bands + trigger points, and document why an adjustment is (or isn’t) required.

- Governance: tax owns policy and arm’s length logic; finance runs calculations and postings; pull in VAT/customs/local controllers for material true-ups.

True-Ups: Mechanics, Invoicing, and Indirect Tax Considerations

Year-end true-ups reconcile budgeted intercompany prices against actual results. They can be executed via price-based adjustments (modifying specific historic transactions) or lump-sum adjustments (a single debit/credit note linked to a transaction type or period).

Symmetry is non-negotiable. Entries must be mirrored in both entities' books, ideally in the same period to avoid FX and timing mismatches. Labels on debit/credit notes must align explicitly with intercompany contracts.

Indirect tax considerations:

- VAT: An upward adjustment on a service fee may require corrections to historic VAT returns. In partially exempt businesses, it can create irrecoverable VAT costs.

- Customs duties: For tangible goods, an upward true-up increases the transaction value, potentially requiring revised import declarations and duty top-ups. Downward adjustments face heavy scrutiny from customs authorities.

Why large true-ups are dangerous: Beyond audit risk (late adjustments can look tax-driven), big post-close true-ups can complicate consolidation tie-outs and Pillar Two/GIR data packages.

Evidence Trail by Transaction Type

The strongest TP policy fails without a contemporaneous evidence trail. Tax managers must retain specific documentation all year:

| Transaction type | Minimum evidence | Where it lives | Common failure mode |

|---|---|---|---|

| Services | Signed service agreement, benefit test documentation, output evidence (deliverables, reports), allocation key workpapers | ICA register, project management system, finance data room | No proof services were actually rendered; missing benefit test |

| IP / Royalties | Executed license agreement, DEMPE analysis, periodic royalty calculation schedules | Legal document management, TP data room | No DEMPE mapping; royalty calculations disconnected from contract base |

| Financing / Guarantees | Loan agreement (signed before funds transfer), standalone credit rating analysis, guarantee fee calculations | Treasury system, TP data room | No credit analysis; agreement executed after funds already transferred |

| Tangible goods | Distribution/manufacturing agreement, pricing documentation, customs valuation declarations | ERP, customs portal, ICA register | Agreements do not reflect actual risk allocation (e.g., states LRD but entity bears inventory risk) |

| Business restructurings | Before/after FAR analysis, DCF or valuation model, termination and new agreements | TP data room, valuation files | No exit charge analysis; missing valuation for transferred intangibles |

4. 2026 Focus Topics: Amount B and Pillar Two Alignment

Amount B Readiness: Scoping, Inputs, and Monitoring

Amount B targets baseline marketing and distribution activities for tangible goods. It is not universal and scoping is tight, so confirm eligibility and the latest tools/FAQs via the OECD’s official Amount B hub.

A practical Amount B workflow (what to actually implement):

- Scope candidates: identify baseline distributors of tangible goods that plausibly fit Amount B.

- Map adoption and counterparties: maintain a jurisdiction-by-jurisdiction view of whether Amount B is available and how it is applied (including symmetry risk with the counterparty).

- Build the input pack: three-year financials, clean segmentation, OpEx classification consistency, and working-capital definitions.

- Run the tool + write a memo: document inputs, exclusions, and why Amount B is or is not applied.

- Monitor outcomes: treat Amount B as an operating control. Track actual vs. target returns and document variances.

Tax departments need a workflow to monitor where Amount B is available and how counterparties will treat it; asymmetry can create double-taxation risk.

Data Alignment: CbCR, TP, and Pillar Two Workstreams

Pillar Two safe harbors and GIR timelines are jurisdiction-specific. Confirm official guidance and align your data early so your TP, CbCR, and GIR packages reconcile cleanly.

Key data alignment controls:

- Post-year-end TP true-ups not reflected in Qualified Financial Statements prior to close can distort GloBE calculations and potentially disqualify from the safe harbor.

- For many calendar-year groups, first GIR filings may be due in 2026 (often June 30, 2026 for FY 2024 filings under transition timing), depending on local implementation.

- MNEs must implement jurisdiction-by-jurisdiction modeling that maps ERP data into a reporting package feeding both TP documentation and the GIR simultaneously.

Use OECD Country Profiles for a Quick Jurisdiction Scan

The OECD Transfer Pricing Country Profiles, updated January 22, 2026, summarize domestic implementation across core topics: the arm's length principle, methods, comparability, intangibles, services, documentation, dispute resolution, and safe harbors.

Use the profiles to verify local documentation requirements, dispute resolution mechanisms, and any simplifications/safe harbors relevant to your footprint.

5. Audit Readiness: Build a Defense File and a 30-Day Response Posture

Defense File Checklist

A defense file goes beyond the Master File, Local File, and CbCR. It compiles the exact evidentiary trail tax authorities will demand during an intensive examination. Build it before an audit is announced.

Core components:

- Reconciliations -- tie tested-party segmented P&L to statutory accounts, tax returns, CbCR, and the Local File.

- Contracts -- signed, dated intercompany agreements (plus amendments) that match operational reality.

- Method memos -- why the method fits the facts (and why alternatives were rejected).

- Benchmark workpapers -- search strategy, accept/reject reasons, data, and calculations.

- Functional analysis evidence -- org charts, process maps, RACI, and decision-making proof.

Production deadlines: Response windows can be tight and penalties can be severe. Treat documentation as audit-ready by the filing date (confirm local rules; in the U.S., a 30‑day production window can apply). See 26 CFR §1.6662-6 for the U.S. standard.

Digital data room: Maintain a centralized, indexed, version-controlled repository. Run a 30‑day drill to confirm you can produce ICAs, benchmarks, tie-outs, and the finalized Local File fast.

Common Audit Pitfalls

- Narrative conflicts between Master File, Local Files, ICAs, and the actual financial outcomes.

- Checkbox functional analysis with no clear link from facts → method selection → results (especially for loss-makers).

- Missing evidence (services without deliverables/benefit test; IP moves without valuation/DEMPE; financing without credit analysis).

- CbCR tie-out gaps that make the numbers look inconsistent across filings and documentation.

- Stale documentation after restructurings, integrations, or major operating model changes.

When to Escalate

Escalate early when the cost of being wrong is high:

- Pre-audit health check: simulated audit review + documentation/data stress test.

- Restructurings and intangibles: supply chain changes, IP migration, or hard-to-value intangibles (DEMPE-driven scrutiny).

- Red flags: persistent losses in high-tax jurisdictions, large unexplained true-ups, material payments to low-tax entities, or rapid restructurings after profitability.

- Certainty tools: consider MAP/APA/ICAP when double-taxation risk or audit exposure is high.

Take the Next Step

Stop scrambling for 2026 transfer pricing compliance. Use this checklist to operationalize Action 13 documentation, OTP monitoring, Amount B scoping, and Pillar Two data readiness.

Take control of your global TP compliance roadmap today:

- Get the actionable roadmap: Download the free 2026 Transfer Pricing Compliance Checklist to map every flow, assign owners, and build an evidence trail you can produce on demand.

- Need help implementing it? Book a call with TPxTAX to pressure-test your current state, identify the biggest compliance gaps, and build a practical 2026 plan across documentation, OTP monitoring, Amount B scoping, and audit readiness.

Sources and further reading (primary first)

- OECD: Action 13 final report landing

- OECD: CbC implementation guidance (PDF)

- OECD: Guidance on Appropriate Use of CbCR data (PDF)

- OECD: Common errors in CbC reports (PDF)

- OECD: Transfer Pricing Country Profiles

- OECD: Pillar One – Amount B

- IRS: Transfer pricing documentation best practices FAQs

- e-CFR: 26 CFR §1.6662-6