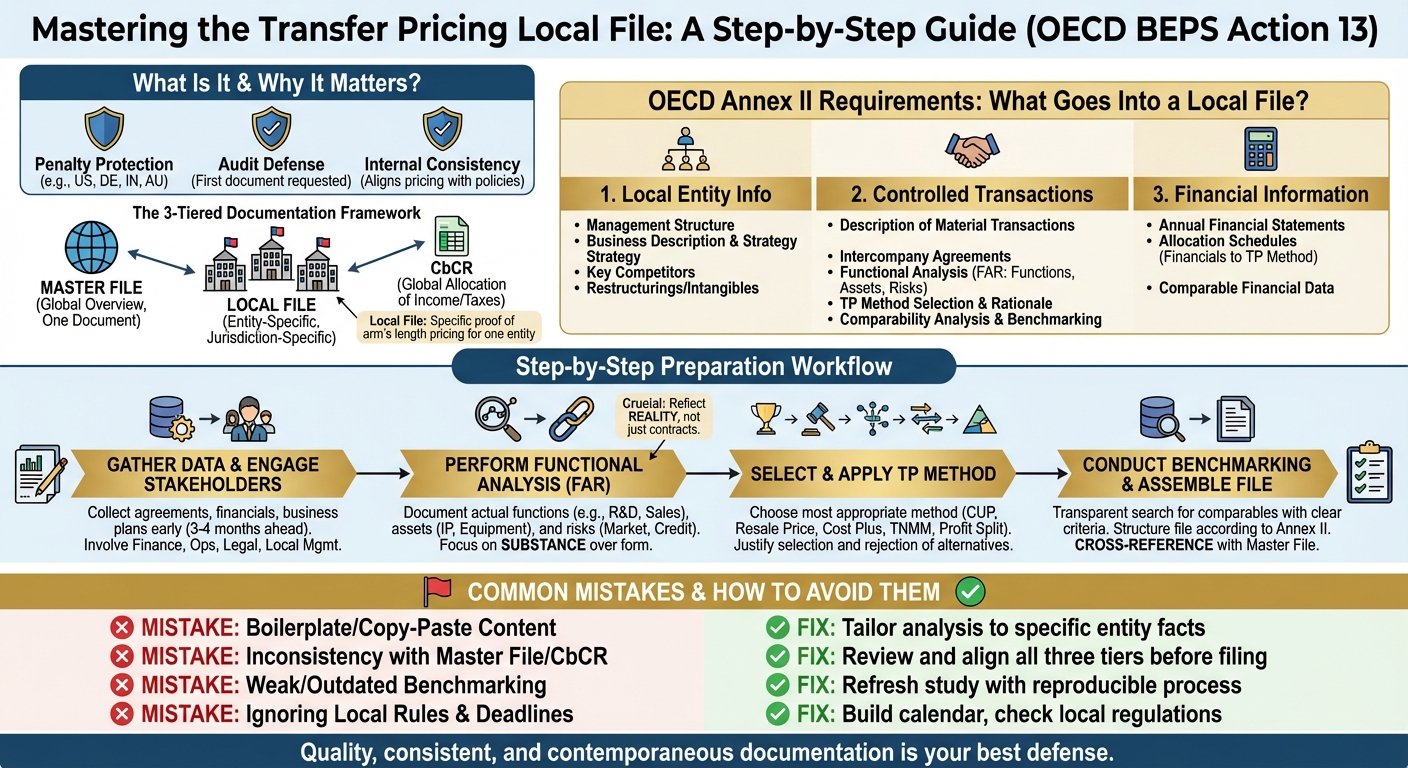

How to Prepare a Local File for Transfer Pricing

The Local File is where your transfer pricing story gets specific. It's the document that proves, entity by entity, that your intercompany transactions are priced at arm's length. And it's the first place tax authorities look when they start asking questions.

Under the OECD BEPS Action 13 framework, every multinational above certain thresholds needs three layers of transfer pricing documentation: a Master File, Local Files, and a Country-by-Country Report. The Local File sits at the core of this structure. It takes the global policies outlined in your Master File and shows exactly how they play out in a specific jurisdiction, backed by functional analysis, a defensible transfer pricing method, and solid financial data.

Getting the Local File right matters. Contemporaneous, well-prepared documentation is directly linked to penalty protection in major jurisdictions like the US, Germany, India, and Australia. Get it wrong, and you're inviting scrutiny, adjustments, and penalties.

This guide breaks down exactly what goes into a Local File, walks you through the preparation process step by step, and highlights the most common mistakes that trip up even experienced TP teams.

What Is a Local File and Why Does It Matter?

A Local File is a transfer pricing document that provides detailed information about a specific entity's intercompany transactions within a single jurisdiction. It serves one core purpose: to demonstrate that the prices charged between related parties comply with the arm's length principle.

The OECD introduced the Local File as part of its three-tiered documentation framework under BEPS Action 13. Here's how the three tiers fit together:

- Master File: A high-level overview of the entire multinational group, covering global operations, organizational structure, intangible assets, financial arrangements, and transfer pricing policies. One document, shared globally.

- Local File: Entity-specific documentation that shows how global TP policies are applied in a particular country. Each entity prepares its own Local File for its jurisdiction.

- Country-by-Country Report (CbCR): A standardized report showing the global allocation of income, taxes paid, and economic activity by jurisdiction.

The Local File supplements the Master File. While the Master File provides context, the Local File provides proof. It focuses on the transfer pricing analysis for transactions between the local entity and associated enterprises in other countries. The Local File also fits within a broader compliance landscape that includes obligations like the Pillar Two global minimum tax, which adds another layer of reporting for large MNEs.

Why does this matter beyond compliance? Three reasons:

- Penalty protection. In jurisdictions like the US, Germany, India, and Australia, having contemporaneous documentation - prepared within the required timeframes - is directly tied to penalty relief. Without it, you lose that protection.

- Audit defense. The Local File is typically the first document tax authorities request during an audit. A well-prepared file can resolve questions early and prevent escalation.

- Internal consistency. The process of preparing a Local File forces you to align your actual intercompany pricing with your stated policies, catching discrepancies before tax authorities do.

Local File vs. Master File

These two documents work together but serve different purposes. Here's a quick comparison:

| Feature | Master File | Local File |

|---|---|---|

| Scope | Entire MNE group (global) | Single entity in one jurisdiction |

| Focus | Global TP policies, organizational structure, intangibles | Specific intercompany transactions and their pricing |

| Content | Business overview, value chain, financial arrangements | Functional analysis, method selection, benchmarking, financials |

| Prepared by | Typically the parent entity or group tax function | Each local entity (often with group support) |

| Purpose | Provides context and the "big picture" | Provides entity-level proof of arm's length pricing |

| Filing | Shared across jurisdictions (one version) | Jurisdiction-specific (one per entity) |

The critical point: these documents must be consistent. If your Master File describes a centralized IP ownership model but your Local File treats the local entity as bearing significant intangible risk, tax authorities will notice. Inconsistencies between the Master File and Local File are one of the most common red flags that invite deeper scrutiny.

What Goes Into a Local File (OECD Annex II Requirements)

The OECD Transfer Pricing Guidelines, Annex II to Chapter V, spell out exactly what a Local File should contain. The requirements fall into three categories: information about the local entity, information about controlled transactions, and financial information.

While local regulations may add country-specific requirements, the OECD Annex II serves as the baseline in most jurisdictions. Sticking closely to this structure is a practical choice - most OECD and G20 countries tell the OECD that their Local File requirements follow this format. For a broader view of what your TP compliance program should cover beyond the Local File, see our transfer pricing compliance checklist.

Part 1 - Local Entity Information

This section sets the scene. Tax authorities need to understand who the local entity is, what it does, and how it fits into the broader group.

What to include:

- Management structure and organization chart. Show the reporting lines within the local entity. Include all major departments, and identify the individuals to whom local management reports, along with the countries where those individuals are based.

- Business description and strategy. Describe what the entity actually does - its products, markets, and business model. Include an indication of whether the entity has been involved in business restructurings or intangibles transfers in the current or prior year. The business strategy should come from actual business or marketing plans, not be written by the tax department after the fact.

- Key competitors. List the major competitors in the local market. Focus on those aspects of competition that are relevant to the comparability factors of the controlled transactions.

A practical tip: the entity description section rarely needs to be more than 1-2 pages. Keep it factual and concise.

Part 2 - Controlled Transactions

This is the heart of the Local File. Tax authorities want to see a complete picture of every material intercompany transaction, along with the analysis that supports the pricing.

What to include:

- Description of material controlled transactions. For each category of transaction (sale of goods, provision of services, licensing, financing, etc.), describe what is being transacted, the business context, and the commercial rationale.

- Amounts involved. Report the intercompany payments and receipts for each transaction category, broken down by tax jurisdiction of the counterpart.

- Intercompany agreements. Provide copies of all material agreements governing the controlled transactions.

- Functional analysis. This is critical. Document the functions performed, assets used, and risks assumed by each party to each transaction. The functional analysis should reflect the actual conduct of the parties, not just what the contracts say.

- Transfer pricing method. Indicate the most appropriate method for each transaction category. Explain why that method was selected and, importantly, why alternatives were not chosen.

- Comparability analysis. Identify the most relevant comparable uncontrolled transactions (internal or external). Describe how you found them, the selection criteria, and any adjustments made to improve comparability.

Part 3 - Financial Information

This section ties the transfer pricing analysis to the numbers that tax authorities can verify.

What to include:

- Annual financial statements. Attach the local entity's financial statements for the fiscal year under review.

- Allocation schedules. Show how the financial data used in applying the transfer pricing method maps to the annual financial statements. This is often the most technically challenging part of the Local File. If you're testing a distribution entity's operating margin, for example, you need to show which revenue and cost lines feed into that calculation.

- Comparable financial data. Provide summary schedules of relevant financial data for the comparable transactions or companies used in your benchmarking analysis.

Here's a reference checklist of the full OECD Annex II requirements mapped to typical data sources:

| OECD Annex II Requirement | Typical Data Source |

|---|---|

| Management structure & org chart | HR / local management |

| Business description & strategy | Business plans, marketing materials |

| Key competitors | Sales / market research team |

| Business restructurings | Corporate development / legal |

| Description of controlled transactions | Finance / operations / contracts |

| Intercompany payment amounts | ERP system / general ledger |

| Intercompany agreements | Legal / group tax |

| Functional analysis (FAR) | Interviews with operations, finance, management |

| Transfer pricing method & rationale | TP team / external advisors |

| Comparables & benchmarking | Commercial databases (e.g., Bureau van Dijk), internal comparables |

| Comparability adjustments | TP team / external advisors |

| Annual financial statements | Finance / statutory audit |

| Allocation schedules (financials to TP method) | Finance / TP team |

| Comparable financial summary data | Commercial databases, public filings |

| Existing APAs or tax rulings | Group tax / legal |

Step-by-Step Guide to Preparing Your Local File

Knowing what goes into a Local File is one thing. Actually preparing one is another. Here's a practical workflow that breaks the process into manageable steps.

Step 1 - Gather Data and Identify Stakeholders

Before you write a single word, you need the raw materials. Start by collecting:

- Intercompany agreements for all material transactions

- Financial data from the ERP system or general ledger, including intercompany payment flows broken down by transaction type and counterparty

- Organization charts showing the local entity's reporting structure

- Business plans and strategy documents from local management

- Prior year Local File and Master File (for consistency and to identify changes)

- Information on any business restructurings, new transactions, or changes in the business model from the prior year

You'll need input from multiple teams. Finance provides the numbers. Operations and sales explain what the entity actually does day to day. Legal provides the agreements. Local management validates the business description and strategy. If you wait until the last minute to chase down these stakeholders, you'll miss your deadline.

On timing: the OECD recommends that the Local File be finalized no later than the tax return filing date for the relevant fiscal year. Many jurisdictions have adopted this standard, and some set earlier deadlines. Start the data gathering process well in advance - ideally 3-4 months before the filing deadline. Our transfer pricing compliance checklist for 2026 can help you track all the documentation milestones across your organization.

Step 2 - Perform the Functional Analysis

The functional analysis is arguably the most important part of the Local File. It describes what each party to a controlled transaction actually does, what assets it uses, and what risks it assumes. This is commonly referred to as a FAR analysis: Functions, Assets, Risks.

Functions to document include:

- Manufacturing, assembly, or procurement

- Sales, marketing, and distribution

- Research and development

- Management and administration

- Quality control

- Logistics and warehousing

- Treasury and financing

Assets to identify include:

- Tangible assets (production equipment, inventory, real estate)

- Intangible assets (patents, trademarks, customer lists, proprietary know-how)

- Financial assets deployed in the business

Risks to assess include:

- Market risk (demand fluctuations, competition)

- Inventory and credit risk

- Currency risk

- Product liability and warranty obligations

- R&D risk (if applicable)

The golden rule here: document the actual conduct of the parties, not just the contractual terms. If a contract says the local entity bears inventory risk but in practice the parent company makes all inventory purchasing decisions, the Local File should reflect the reality. Tax authorities increasingly focus on substance over form, and a Local File that contradicts actual operations is worse than no file at all.

Use process flow diagrams where they help. A visual showing how goods flow from manufacturer to distributor to customer, with the associated functions and risks at each stage, can communicate more than several pages of text.

Step 3 - Select and Apply a Transfer Pricing Method

The OECD recognizes five transfer pricing methods. Your Local File must indicate which method you've selected for each transaction category, why it's the most appropriate, and why alternatives were not suitable.

| Method | How It Works | Best For |

|---|---|---|

| Comparable Uncontrolled Price (CUP) | Compares the price in a controlled transaction to the price in a comparable uncontrolled transaction | Commodity trades, licensing with public rate data |

| Resale Price Method | Starts with the resale price to an independent party and subtracts an appropriate gross margin | Distribution activities |

| Cost Plus Method | Adds an appropriate markup to the costs incurred by the supplier | Manufacturing, intra-group services |

| Transactional Net Margin Method (TNMM) | Compares the net profit margin of the tested party to margins earned by comparable independent companies | Most common method globally; broad applicability |

| Profit Split Method | Splits the combined profit from a transaction based on each party's relative contribution | Highly integrated operations, unique intangibles on both sides |

When selecting a method, consider:

- Availability of reliable comparables. CUP is the most direct method, but it requires closely comparable uncontrolled transactions. If those don't exist, a one-sided method like TNMM is often more practical.

- The nature of the transaction. Simple distribution? Resale Price or TNMM. Contract manufacturing? Cost Plus or TNMM. Unique, highly integrated value chain? Profit Split may be the only option.

- The tested party. One-sided methods require selecting the "less complex" party as the tested party. Document why you chose the tested party you did.

Your Local File should explicitly discuss why the selected method is the most reliable for each transaction, and briefly explain why other methods were considered and rejected.

Step 4 - Conduct a Benchmarking Study and Assemble the File

The benchmarking study identifies comparable uncontrolled transactions or companies that validate your transfer pricing results.

For external benchmarking (most common):

- Define the search criteria (industry codes, geography, independence, size, financial data availability)

- Run the search in a commercial database (Bureau van Dijk's Orbis/TP Catalyst, S&P Capital IQ, or similar)

- Apply quantitative screens (revenue thresholds, financial data availability, consecutive years of data)

- Review the remaining companies qualitatively (reject those with non-comparable business models, unusual financial events, or insufficient public information)

- Document every step of the search process, including the reasons for rejecting companies at each stage

Tax authorities scrutinize the benchmarking process closely. A defensible search means a transparent, reproducible process where the selection criteria are clearly stated and consistently applied.

Assembling the final document:

Once all components are ready, structure the Local File following the OECD Annex II framework:

- Introduction (scope, purpose, structure of the report)

- Local entity description (management, business, strategy, competitors)

- Controlled transactions (descriptions, FAR analysis, method selection, benchmarking)

- Financial information (financial statements, allocation schedules, comparable data)

- Appendices (intercompany agreements, org charts, benchmarking search screenshots, APAs or rulings)

Before finalizing, cross-reference your Local File against the Master File. The entity characterization, transaction descriptions, and TP policies should align. If they don't, either the Master File or the Local File needs to be updated.

Common Mistakes and How to Avoid Them

Even experienced TP teams make avoidable errors in their Local Files. Here are the most frequent pitfalls, along with practical fixes.

| Mistake | Consequence | How to Fix It |

|---|---|---|

| Boilerplate/copy-paste content | Tax authorities flag generic content as a red flag inviting deeper scrutiny | Tailor each Local File to the specific entity and jurisdiction |

| Inconsistency between Local File and Master File | Triggers audit questions and undermines credibility | Cross-reference both documents before finalizing |

| Missing or weak comparability analysis | Cannot justify arm's length compliance to tax authorities | Invest in a proper benchmarking study with transparent methodology |

| Not reflecting actual business operations | Documentation fails the substance-over-form test | Base the FAR analysis on interviews and real operations, not just contracts |

| Ignoring local regulatory requirements | Non-compliance with country-specific rules, potential penalties | Check each jurisdiction's TP documentation rules beyond the OECD baseline |

| Missing filing deadlines | Loss of penalty protection | Build an internal calendar tracking deadlines by jurisdiction |

Documentation Pitfalls

Boilerplate content is the most common mistake. Tax authorities can spot a copied-and-pasted Local File from a mile away. If your Brazilian entity's business description reads identically to your German entity's, that's a problem. Each Local File should reflect the specific facts and circumstances of the local entity. Use the same framework and methodology, but customize the substance.

Inconsistency between tiers. Your Master File says the group follows a centralized principal model. Your Local File describes the local entity as an "entrepreneur" bearing significant risks. That contradiction is exactly what tax auditors are trained to spot. Before submitting any Local File, verify that:

- Entity characterizations match across Master File and Local File

- Transaction descriptions are consistent

- TP policies described at the group level match the methods applied locally

- Financial data referenced in the Local File reconciles with the CbCR

Weak comparability analysis. Stating that you used TNMM and referencing a handful of comparable companies is not enough. Tax authorities expect a documented, step-by-step search process with clear selection and rejection criteria. If your benchmarking study is several years old and you haven't refreshed it, that's another red flag.

Contracts vs. reality. The OECD emphasizes that the actual conduct of the parties should take precedence over contractual terms when they diverge. If your contract says the local entity bears inventory risk, but the parent company actually controls inventory levels and purchasing decisions, your functional analysis needs to reflect the reality. Preparing a Local File based on contractual terms alone, without verifying actual operations, is a common and costly mistake.

Local regulation variations. While most OECD and G20 countries base their documentation requirements on the OECD Annex II framework, many add country-specific rules. Some jurisdictions require additional disclosures, different formats, or supplementary forms. Always check the local requirements for each jurisdiction where you file. The OECD standard is the floor, not the ceiling. If you operate in Germany, for example, understanding the specific requirements around German transfer pricing audits is critical to staying ahead of enforcement changes.

Missed deadlines. In most jurisdictions, the Local File should be ready by the tax return filing date. Some countries require earlier submission. Missing these deadlines doesn't just risk penalties - it eliminates your penalty protection. Build a compliance calendar that tracks documentation deadlines for every jurisdiction where the group operates.

Key Takeaways

Preparing a Local File is not just a compliance exercise. Done well, it's your best defense in a transfer pricing audit and a tool for ensuring that your intercompany pricing holds up under scrutiny.

Here's what to take away:

- Start with the OECD Annex II framework. It defines the three categories of required content: local entity information, controlled transactions, and financial information. Most jurisdictions follow this structure, so it's the safest starting point.

- Begin data gathering early. Don't wait until the filing deadline is approaching. Coordinate with finance, operations, legal, and local management well in advance. The hardest part is usually getting the right data from the right people on time.

- Invest in the functional analysis. The FAR analysis (functions, assets, risks) is the foundation of your entire transfer pricing argument. Base it on what actually happens, not just what contracts say.

- Document your method selection thoroughly. Explain why you chose the method you did, and why alternatives were not suitable. Tax authorities expect this reasoning, not just a conclusion.

- Make your benchmarking defensible. A transparent, step-by-step search process with clear criteria is far more valuable than a long list of comparable companies with no explanation of how they were selected.

- Check consistency across tiers. Cross-reference your Local File with the Master File and CbCR before submission. Inconsistencies are one of the top audit triggers.

- Respect local rules and deadlines. The OECD framework is the starting point, but each jurisdiction may add its own requirements. Build a compliance calendar and track deadlines proactively.

The bottom line: quality documentation beats volume. A concise, well-supported Local File that reflects actual business operations will serve you better than a 200-page document full of generic descriptions and stale benchmarking data.